A Precise Overview Of The Steps Involved In The KYC Process

In the complex realm of financial services, KYC (know your customer) compliance is crucial in ensuring the integrity of operations. Not just a regulatory necessity, KYC is a shield against fraud and a cornerstone of global anti-money laundering efforts.

In this article, we’ll cover the essential KYC process steps, unraveling the meticulous journey financial institutions undertake to authenticate their clients. We’ll dive into the intricacies of customer acceptance policies, identification procedures, due diligence, and ongoing monitoring.

We’ll also uncover KYC’s pivotal role for platform operators and users alike—fortifying trust, security, and regulatory adherence in the financial landscape. Let’s get started.

What is KYC (know your customer)?

KYC, or know your customer, is how financial institutions validate their clients’ identity and potential risks. KYC has evolved as a response to escalating threats of fraud, money laundering, and terrorism financing. Rooted in the imperative to establish a secure financial environment, KYC verification has become synonymous with regulatory compliance for financial institutions worldwide.

The KYC verification process isn’t just a best practice but a legal requirement imposed by regulatory bodies worldwide. Financial institutions adhere to established protocols to meet regulatory standards, such as the customer identification program (CIP) in the United States. These frameworks ensure KYC processes are robust, consistent, and aligned with global efforts to curb illicit financial activities.

The importance of know your customer in today’s world

For any financial organization, KYC is the only real guardian against the multifaceted threats of today’s financial landscape. Let’s look at what KYC does for financial institutions.

Preventing identity theft

Central to KYC is the robust verification of a customer’s identity, creating a bulwark against identity theft. In a world rampant with sophisticated scams, ensuring individuals are who they claim to be is foundational to the security of financial transactions.

Mitigating fraud risks

Financial institutions navigate a landscape fraught with ever-evolving fraud risks. The KYC process acts as a dynamic shield, incorporating customer due diligence and thorough scrutiny of financial transactions. Doing so is a proactive measure to identify and mitigate potential risks before they escalate.

Complying with regulations

Proper KYC verification processes aren’t just a good idea—it’s a legal imperative. Financial institutions must implement KYC measures to comply with global regulations such as anti-money laundering (AML) requirements.

Protecting the reputation of businesses

Beyond regulatory compliance, KYC safeguards businesses’ reputations. A robust KYC framework assures customers and stakeholders that financial institutions are committed to ethical practices. This commitment fortifies trust and shields businesses from the reputational fallout of potential involvement in financial crime.

Key compliance and regulation considerations

In the relentless battle against financial crimes, understanding the legal landscape is paramount for financial institutions. Legal frameworks and several regulatory bodies globally define the KYC process.

The legal framework guiding KYC processes

At the forefront of KYC procedures is the legal bedrock that underpins its existence. Financial institutions operate within a framework shaped by laws such as the Bank Secrecy Act (BSA). Enacted in 1970, the BSA laid the foundation for modern KYC practices, requiring financial institutions to keep records of cash purchases, report large transactions, and identify and report suspicious activities.

Additionally, the USA PATRIOT Act of 2001 reinforced the KYC mandate, compelling banks to establish a customer identification program (CIP). This program necessitates the verification of customer identities through document verification and data, emphasizing the critical role of identity verification in the fight against money laundering and other financial crimes.

Regulatory bodies monitoring KYC compliance

The vigilance over KYC compliance extends beyond individual financial institutions. Regulatory bodies play a pivotal role in shaping and monitoring the effectiveness of KYC processes. These bodies, from national entities to international organizations, ensure financial institutions adhere to the prescribed standards.

One of the most prominent international organizations regulating KYC is the Financial Action Task Force (FATF), which sets global standards for anti-money laundering (AML) and counter-terrorist financing (CTF) efforts. Its recommendations guide jurisdictions in establishing effective KYC procedures. Nationally, bodies like the Financial Crimes Enforcement Network (FinCEN) in the United States enforce AML regulations and oversee the implementation of KYC processes.

Steps involved in the KYC process

Proper KYC procedure involves a systematic approach, essential for financial institutions aiming to navigate the complexities of regulatory compliance and mitigate financial risks. Let’s review the steps involved.

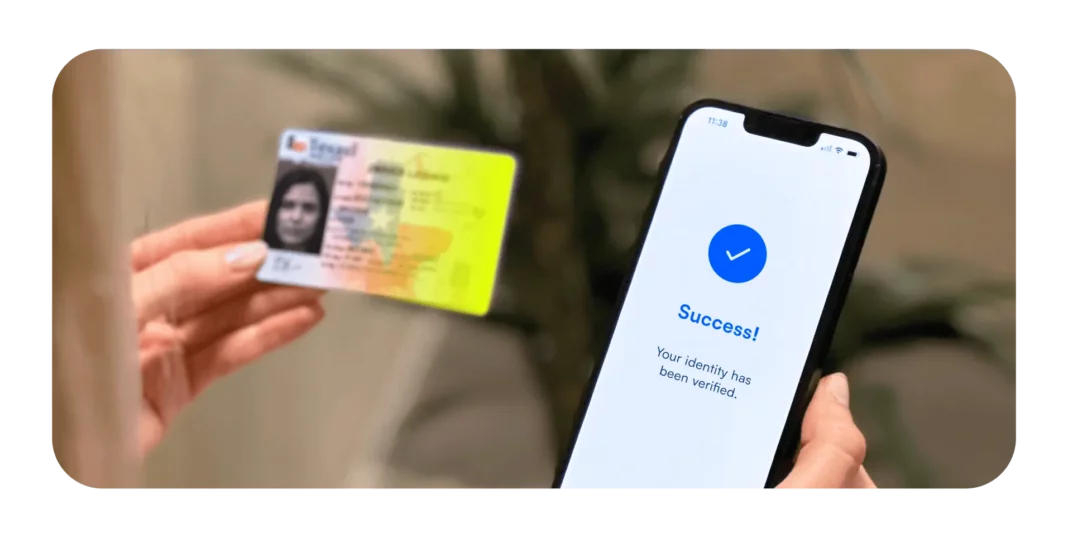

1. Customer identification program (CIP)

The foundation of the KYC process rests on a robust customer identification program (CIP). This initial phase, conducted during the customer onboarding process, involves:

- Collection of basic information: Gather fundamental details such as name, date of birth, address, and identification number.

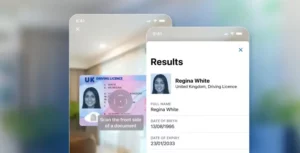

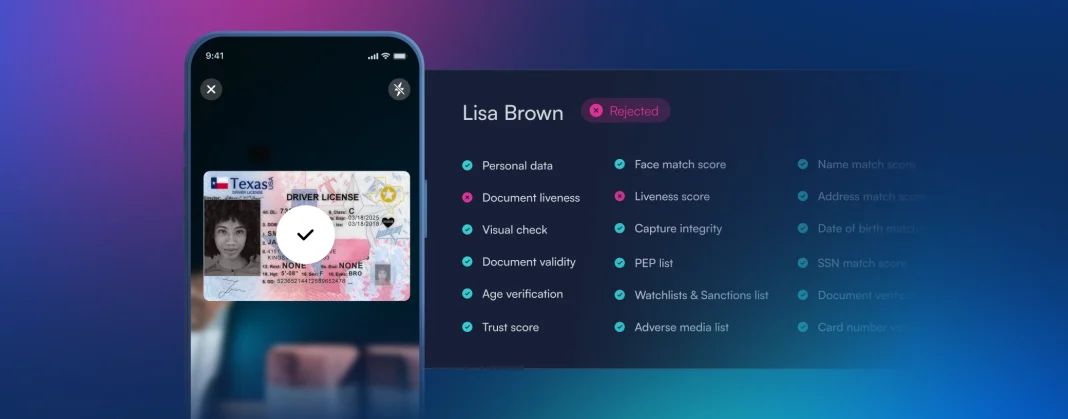

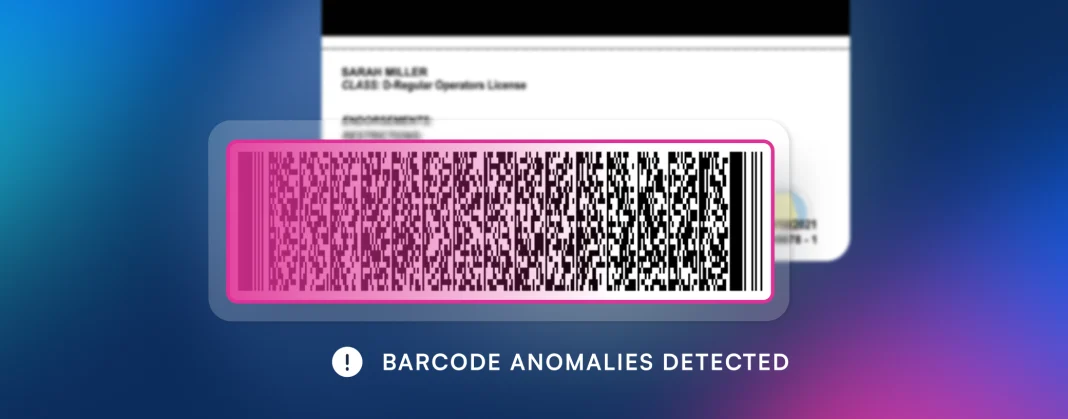

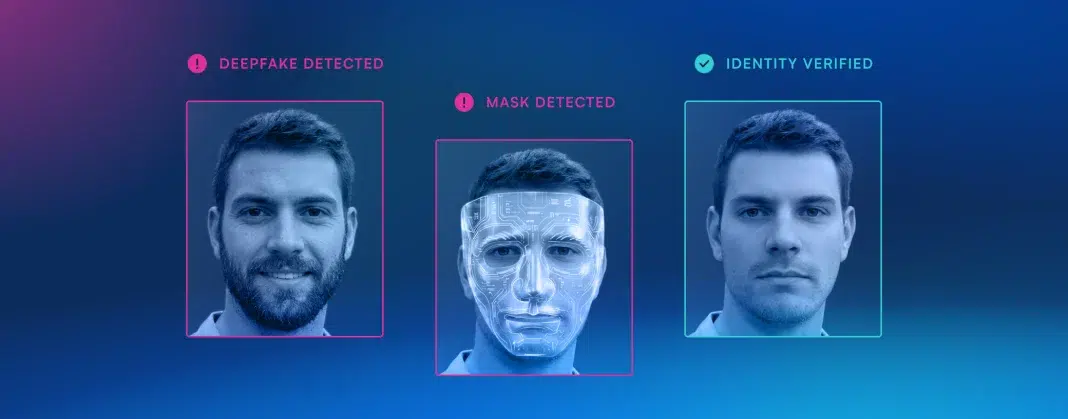

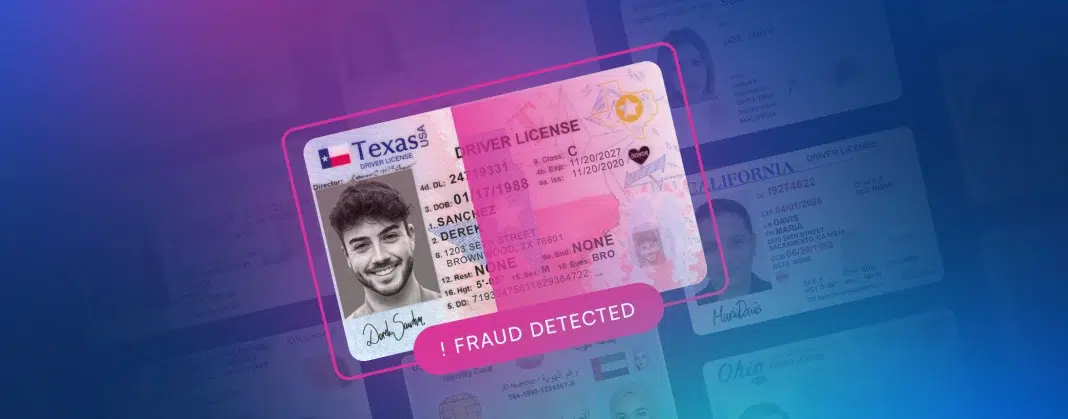

- Verification of identity documents: Authenticate the customer’s identity through government-issued KYC documents like passports or driver’s licenses.

- Screening against watchlists: Conduct screenings to ensure the customer is not associated with illicit activities or on global watchlists.

2. Customer due diligence (CDD)

Diving deeper into understanding the customer, customer due diligence (CDD) is a pivotal stage that includes:

- Understanding the nature of customers’ activities: Gain insights into the customers’ business or financial activities to assess the level of risk.

- Assessing the source of funds: Scrutinize and verify the origin of funds to detect any suspicious transactions.

- Ongoing monitoring of customer transactions: Establish continuous surveillance of customer transactions to promptly identify and respond to anomalies.

3. Enhanced due diligence (EDD)

For higher-risk customers, enhanced due diligence (EDD) becomes imperative. This process involves:

- Triggering factors for EDD: Define specific criteria, such as unusual transactions or business activities, that trigger the need for enhanced scrutiny.

- Gathering additional information for high-risk customers: Collect comprehensive data, including business certificates, board members’ identities, and on-site visit reports.

- Periodic review and update of EDD information: Ensure EDD information is regularly reviewed and updated to reflect any changes in the customer’s risk profile.

4. Ongoing monitoring and risk assessment

Continuing vigilance is essential in the dynamic landscape of financial transactions. This involves:

- Determining customer risk profiles: Classify customers based on their risk levels, considering factors like transaction volume and business type.

- Categorizing customers based on risk: Group customers into risk categories to streamline monitoring efforts.

- Assigning risk levels for enhanced due diligence: Allocate risk levels to facilitate applying enhanced due diligence procedures based on the assessed risk.

By comprehensively navigating these KYC due diligence procedures, financial institutions not only ensure compliance with KYC regulations but also fortify their defenses against financial crimes and fraudulent activities.

Challenges in the KYC process

Navigating the KYC process is not without its hurdles. Financial institutions face challenges with KYC that call for strategic solutions.

Balancing security and customer experience

The perpetual challenge in KYC lies in balancing stringent security measures and a seamless customer experience. While robust security protocols are imperative to mitigate financial risks and prevent fraudulent activities, overly intricate verification processes can lead to user dissatisfaction and potential abandonment. Institutions face the arduous task of implementing security measures that are both effective and user-friendly, ensuring compliance without compromising the ease of customer onboarding.

Keeping up with evolving regulations

In the ever-evolving landscape of financial regulations, staying abreast of changes is challenging for institutions engaged in KYC compliance. The regulatory environment is dynamic, with amendments and additions occurring frequently. Financial organizations must adapt their existing KYC procedures to align with new regulations and stay proactive in anticipating forthcoming changes.

The capacity to swiftly incorporate regulatory updates into existing frameworks is essential to avoid compliance lapses and potential legal repercussions. That’s why most financial institutions partner with a KYC solution provider that stays abreast of changes.

Managing the cost of compliance

The financial commitment associated with KYC compliance poses a substantial challenge for institutions, particularly when weighed against budgetary constraints. The KYC process demands substantial human resources for tasks such as document verification, risk assessments, and ongoing monitoring.

The costs extend beyond personnel to encompass technology investments in automation tools and AI-driven solutions. Striking a balance between effective compliance and cost efficiency becomes a strategic imperative, requiring institutions to invest judiciously in technologies that streamline the KYC process without undue financial strain.

Addressing these challenges requires a holistic approach, combining technological innovation, strategic foresight, and a commitment to providing a positive customer experience.

Know your customer: More than just best practice

Traversing KYC’s intricate path, from initial identification to ongoing monitoring, reveals its pivotal role in sustaining financial trust. KYC is not just best practice; it’s a regulatory necessity—the key to fortifying security and fostering customer satisfaction. Looking forward, KYC should adapt to emerging trends, becoming a mandate and a strategic differentiator.

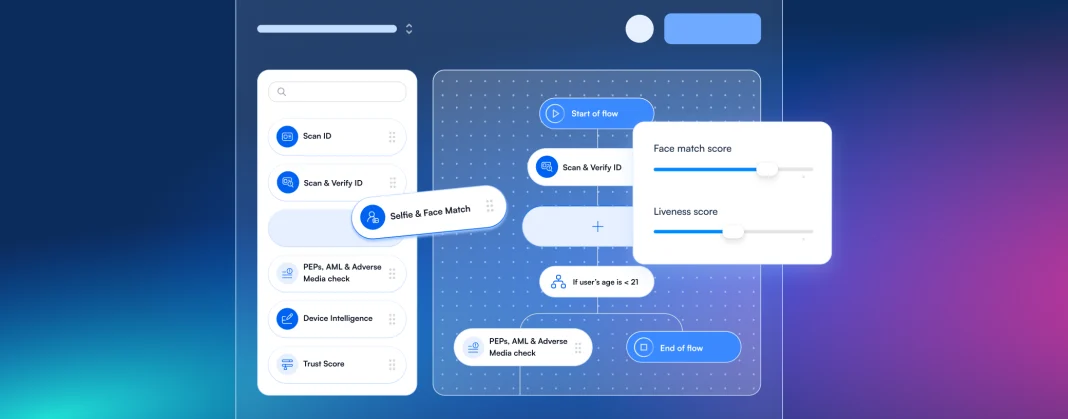

How Microblink can help: Automate KYC verification

KYC can be costly and time-consuming. Our job at Microblink is to make it more efficient by providing automated KYC solutions. Built by people, used by humans, but leveraging AI-powered tech, we build verification processes that really work. That means you can trust your customers, and they can trust you.