Customer Due Diligence for Banks: Risk Management and Compliance

Banks of all stripes need to conduct customer due diligence (CDD) as part of their daily operations. Understanding who they’re working with and what their customers are doing is essential to protecting all stakeholders in the business relationship.

The two main reasons banks and financial institutions need to concern themselves with due diligence—and CDD specifically—are risk management and compliance. Through CDD, banks can assess the risks associated with their customers and take appropriate measures to mitigate them.

In this post, we’ll cover why CDD matters and how to implement it efficiently.

Why is due diligence important for banking?

Simply put, banks need to know their customers. They need to know who they are and that they’re representing themselves accurately. Banks also need assurance that customers aren’t using their accounts for criminal activities, like money laundering.

This applies to fintech firms and neobanks as well. The Federal Reserve publishes a guide on due diligence processes for financial technology, noting the challenges and urgency that come with the territory. Due diligence is especially critical because of the speed with which fintech can compile massive amounts of sensitive data.

The importance of CDD in risk management

These analyses create a risk profile or ranking that informs all elements of account management. For example, how much scrutiny is applied to transactions is proportionate to an account’s risk.

The importance of CDD in compliance

CDD is a requirement in several intertwined regulations applicable to banks, including:

- The Bank Secrecy Act (BSA): The BSA prescribes several requirements that protect bank customers and prevent financial crimes. The CDD Rule expanded the scope of the BSA to explicitly require verification and ongoing monitoring.

- The USA PATRIOT Act: The Uniting and Strengthening America by Providing Appropriate Tools Required to Intercept and Obstruct Terrorism Act is focused on exactly what its name says; it leverages CDD to prevent terrorist financing.

- Know your customer (KYC) and anti-money laundering (AML): These are general standards that specific laws (see above) prescribe rules for. Organizations need to abide by BSA, PATRIOT, and other frameworks to meet them.

Understanding the CDD process flow

Given how critical CDD is to a bank’s risk-based approach and regulatory compliance management, it’s important to have an effective process in place. Every lead and customer needs to be verified and evaluated before—and after—they’re onboarded.

If you’re asking when KYC processes should be performed, it’s not one-and-done; they need to be ongoing throughout customer relationships with a financial institution.

That process generally includes all of the following stages.

Collecting customer information

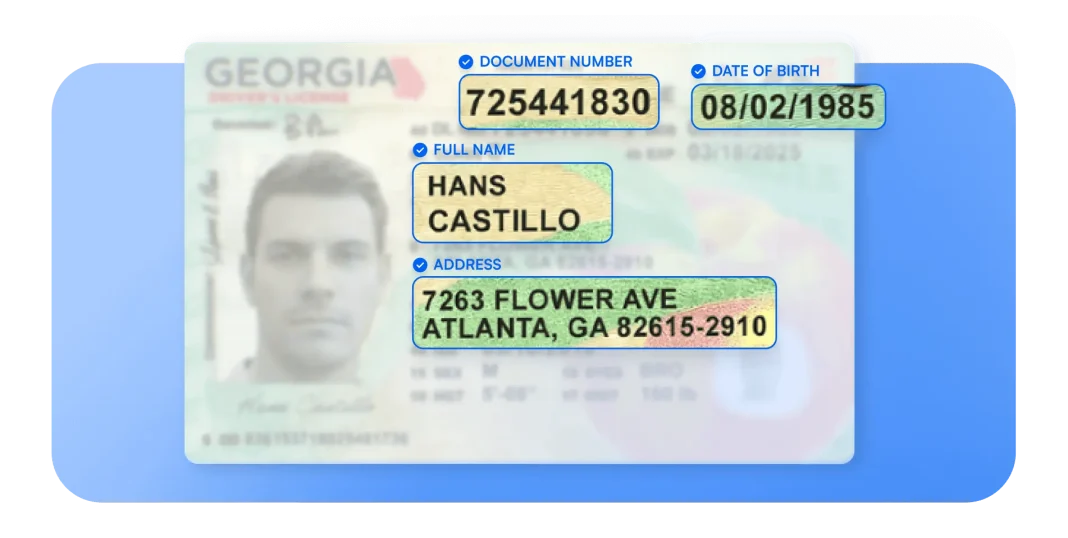

Banks need to collect specific information from potential customers before opening their accounts. The Customer Identification Program (CIP) calls for:

- An individual’s or business’s name

- An individual’s date of birth

- An address

- An identification number, such as:

- A taxpayer ID number

- A passport or license number

- A government photo ID number

These are the bare minimum pieces of information that must be present before an account is opened—a preliminary customer due diligence for banks checklist.

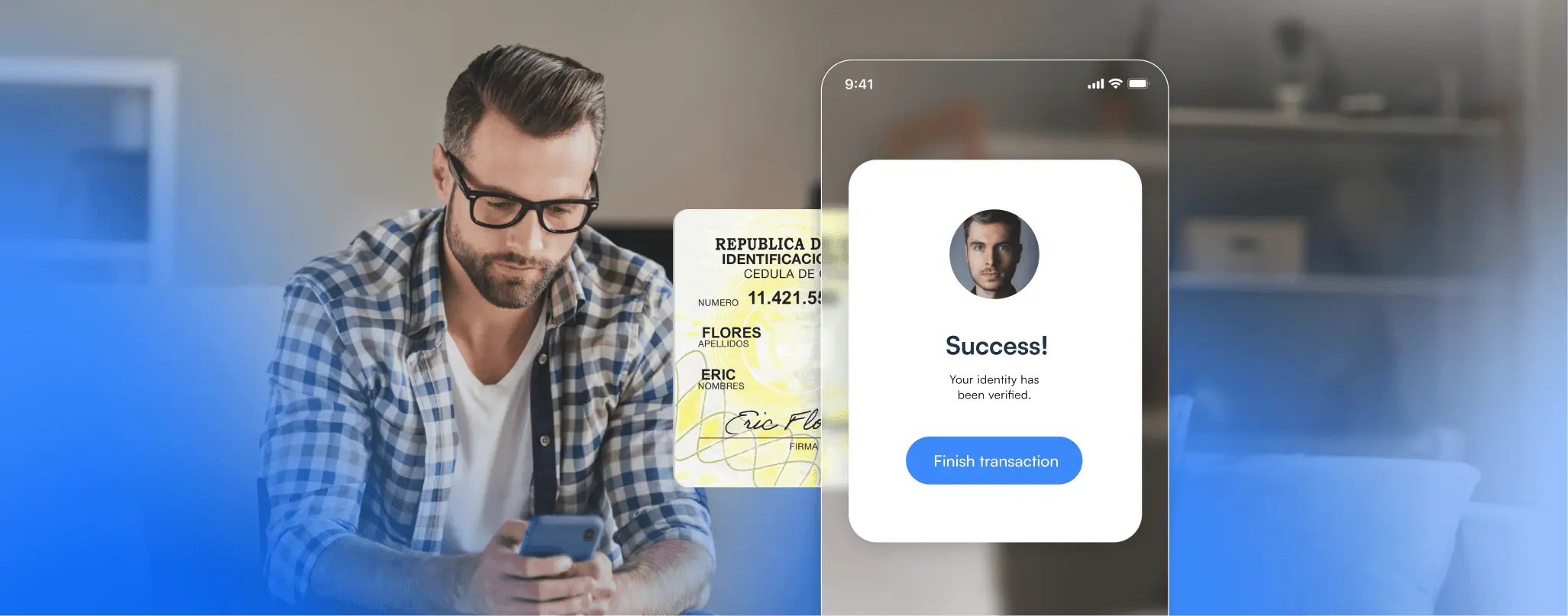

Verifying customer information and identity

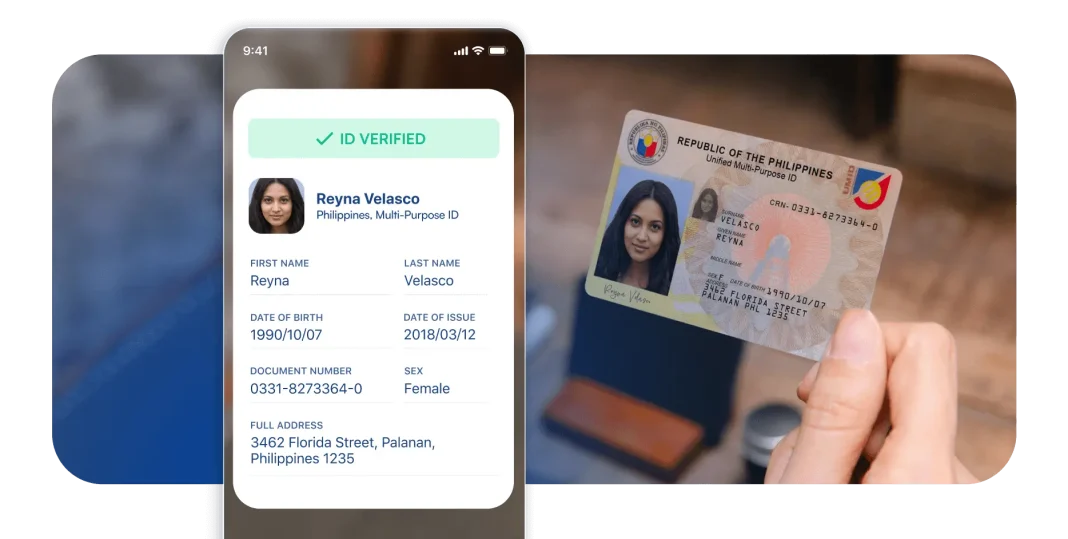

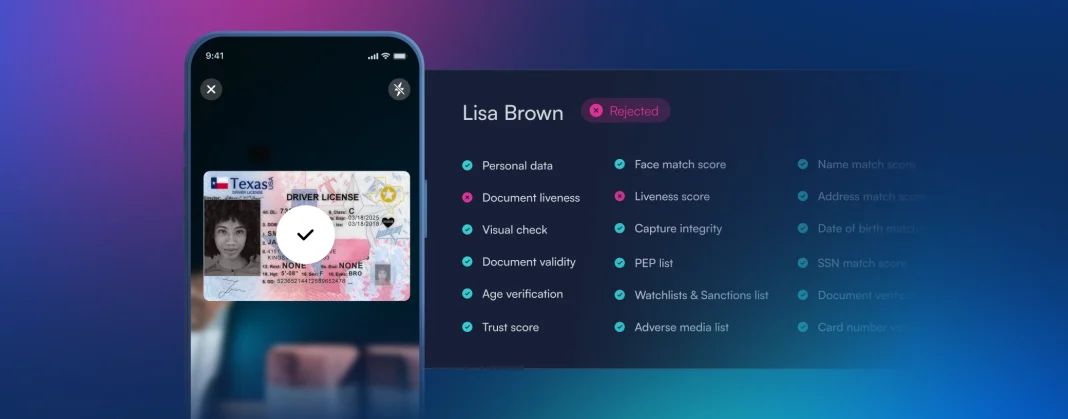

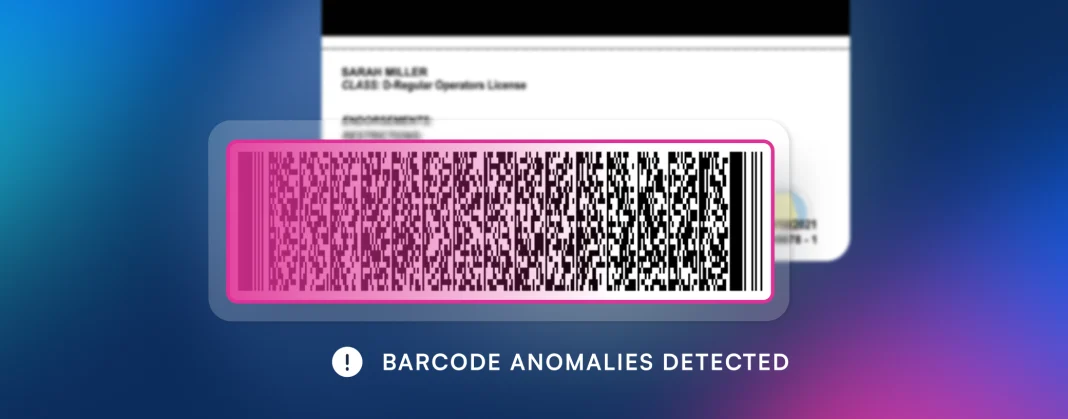

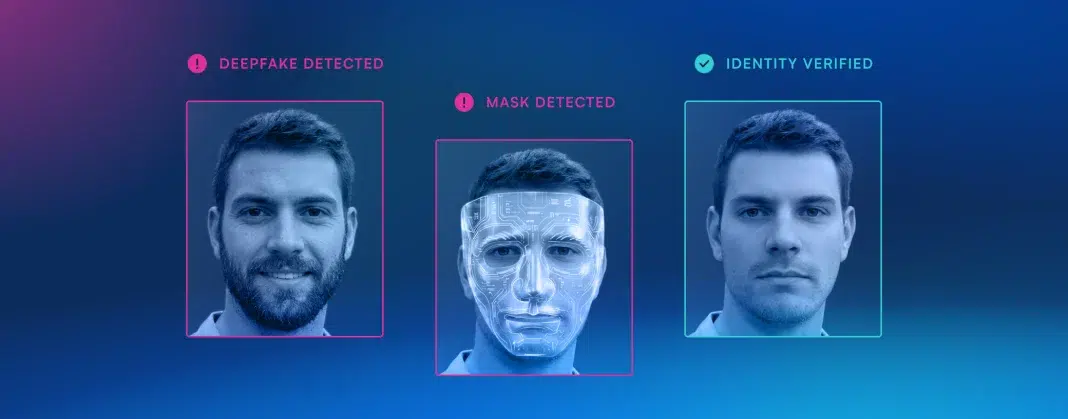

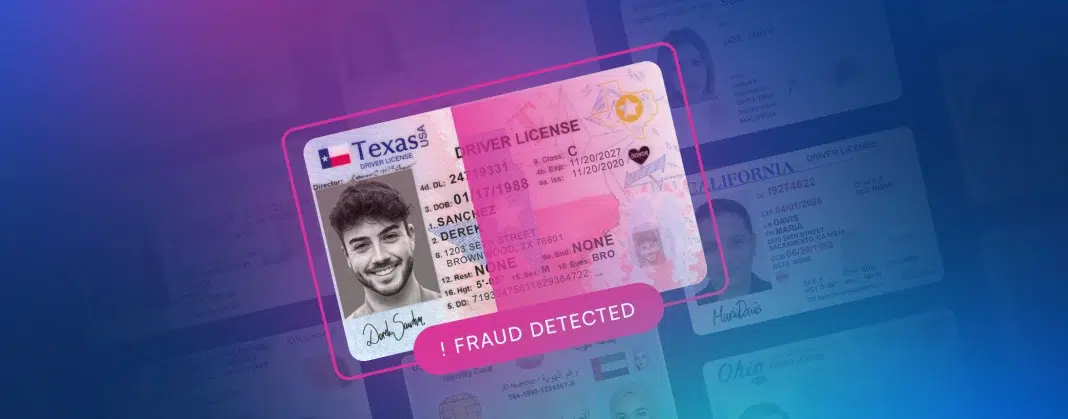

Once information has been collected, banks need to verify that it is accurate and legitimate. The most important part of KYC ID verification is scanning documents submitted to ensure they’re not false. Digital scanners can compare ID cards, for example, against templates or databases to guarantee their authenticity.

Discrepancies between information on the documents and information submitted elsewhere (i.e., chosen names or outdated addresses) need to be flagged and reviewed. They may delay account creation or impact a customer’s risk profile.

Analyzing risk and assigning risk scores

Banks use it after collecting and verifying information to analyze an account and determine its risk. BSA risk assessment uses categories such as:

- Risks of or related to money laundering

- Risks of or related to terrorist financing

- Risks of or related to account misuse

The relative likelihood that a customer’s account would be used for these determines their risk score, which is subject to change over time based on customer behavior.

Enhanced due diligence in financial services

Enhanced due diligence (EDD) increases the CDD protocols for one or more customers because of greater risk, either actualized or suspected.

For example, if a bank’s standard KYC verification process suggests that a potential customer carries more risk than is expected or desired, the bank might collect more information from and on them than it does for other customers. It might require intensive document vetting or greater scrutiny when approving transactions.

Ongoing monitoring, investigation, and reporting

Importantly, identity verification for banks is not a finite process. Banks cannot just collect and verify customers’ information once at account startup. Instead, they must continuously monitor accounts and re-verify a customer’s identity.

This also includes monitoring account transactions and flagging any irregular or otherwise suspicious activity. A customer whose risk score is generally low might trigger re-classification if they start engaging in potentially risky behavior—for example, if an organization suddenly switches to cash transaction structuring.

What solutions are available for effective CDD?

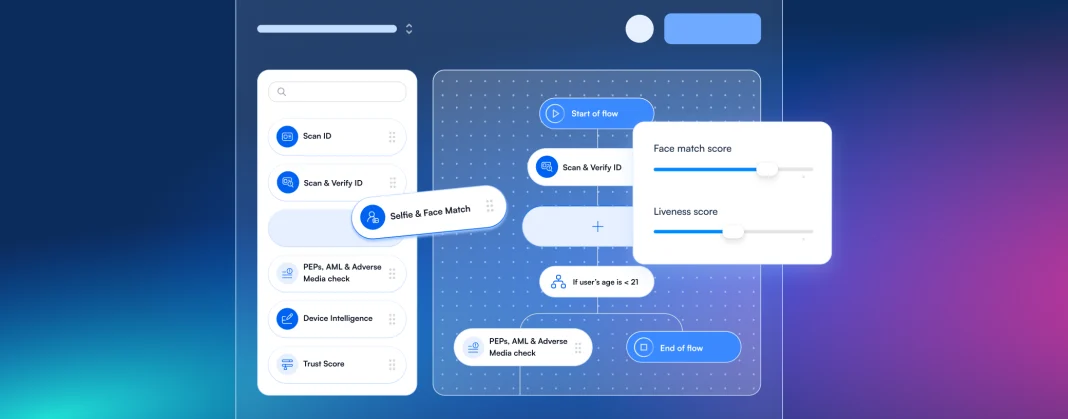

Most banks rely on digital solutions for some or all aspects of CDD. The most effective tools tackle several steps at once or integrate seamlessly with a firm’s tech stack.

Some customer due diligence solutions banks should consider are:

- Automated verification, aided by artificial intelligence (AI)

- Tools for risk monitoring, analysis, and cross-channel alerts

- Dynamic risk profiles that update automatically and in real-time

- Transaction analysis tools that flag and address suspicious activity

In general, anything you can do to automate processes will benefit your CDD efforts.

How Microblink Can Help

Ultimately, meeting global KYC standards and other regulations can be challenging for many banks and financial institutions. Care and attention to detail throughout the process can strain internal resources and reduce bandwidth for other operations.

Microblink facilitates CDD with innovative, AI-driven solutions that automate ID capture, verification, and assist with ongoing risk monitoring. Our tools empower banks to maximize efficiency while minimizing friction for their customers.

Optimize your CDD processes with automation to take your risk management and compliance to the next level.